In November 2026, the new EU Waste Shipment Regulation (WSR) will fully ban the export of plastic waste to non-OECD countries. At that time, millions of tonnes of low-grade plastic waste annually will no longer be eligible for transboundary shipment and disposal, and must be treated and recycled within the EU. For plastic recycling enterprises, deploying pyrolysis capacity at this stage allows them to leverage the market gap created by this policy to establish technological and scale advantages. This aligns with global environmental policy directions and offers clear value in industrial upgrading and commercial implementation.

1. Policy Background: Waste Shipment Regulation

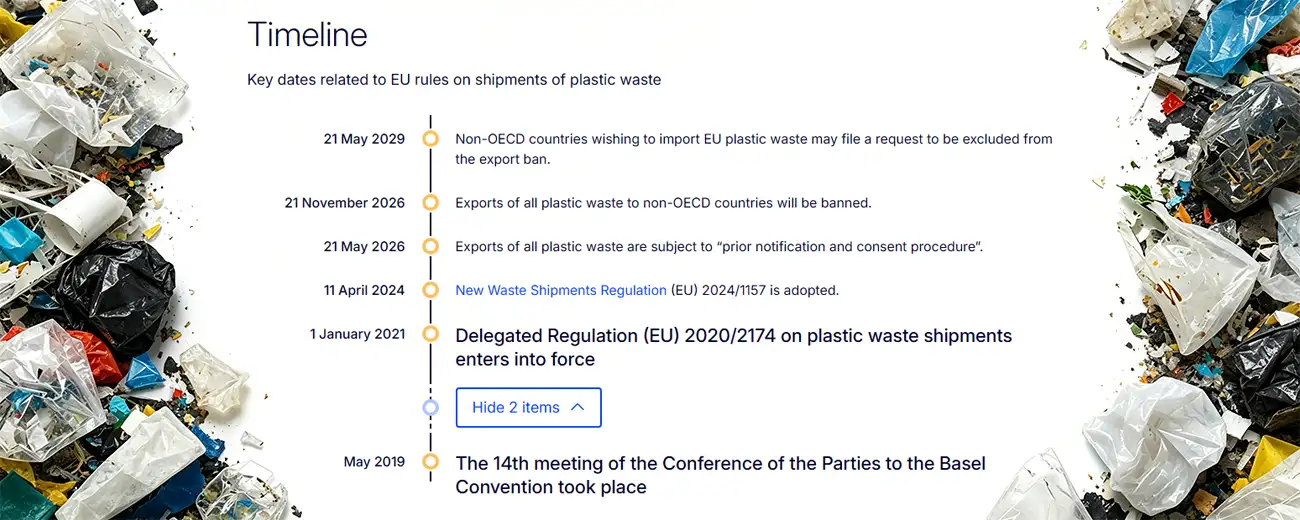

1.1 Core Content of the WSR Amendment

- From 21 May 2026: Exporting plastic waste, including clean, non-hazardous waste (which is destined for recycling) (B3011) will be subject to the “prior notification and consent procedure”.

- From 21 May 2027: Exporters of plastic waste, similarly as in the case of other waste, have to demonstrate that the waste exported is properly managed in the facility located in the recipient country to which it is shipped. Therefore, they must ensure that independent audits are carried out in such facilities, demonstrating that these facilities manage waste in an environmentally sound manner.

- From November 21, 2026 to May 21, 2029: There will be a complete ban on such exports to non-OECD countries. After this period, non-OECD countries interested in importing plastic waste are invited to notify the European Commission and demonstrate their capacity to manage such waste in an environmentally sound manner, in order to be included in the list of non-OECD countries to which plastic waste may be exported from the EU.

1.2 Reasons for Policy Introduction

- Environmental Justice: The EU has long exported large volumes of waste plastic to Southeast Asia, Africa, and other regions, causing severe local pollution and ecological harm, drawing sustained criticism from international environmental organizations. The new regulation directly responds to this model of waste colonialism.

- Spillover effect of China’s “National Sword” policy: Following China’s ban on imported waste plastic in 2018, many Southeast Asian countries also tightened or prohibited imports. This forced the EU to recognize that relying on third countries for waste disposal is unsustainable.

- Circular Economy Action Plan: The EU’s Circular Economy Action Plan 2.0 stipulates that all packaging plastic in the EU must be recyclable or reusable by 2030. Continuing large-scale exports of waste plastic would prevent the EU from monitoring actual recovery rates and hinder the achievement of its circular economy targets.

2. Market Fundamentals: Feedstock Surplus and Downstream Needs

2.1 Supply Side: Abundant Waste Plastic Feedstock

Following the implementation of the EU WSR Regulation in 2026, approximately 500,000 to 800,000 tons of waste plastic previously exported annually must be processed locally. This will widen the gap in regional treatment capacity. Consequently, a plastic pyrolysis plant compliant with EU environmental regulations can generate sustained returns.

2.2 Demand Side: Chemical Giants’ Green Needs

The PPWR mandates mandatory recycled content ratios for plastic packaging by 2030. Petrochemical giants like BASF, Shell and TotalEnergies are sourcing large-volume ISCC PLUS certified pyrolysis oil for production blending to meet statutory recycling quotas. Robust downstream demand provides a stable profit guarantees for plastic pyrolysis project investments.

3. Timing Analysis: Why Now Is the Best Opportunity to Deploy Pyrolysis Plant

Securing policy dividends hinges on construction progress. Generally, for large-scale pyrolysis facilities, the entire development cycle from project initiation to Commercial Operation Date (COD) spans 12 to 18 months.

2026 presents a prime window for pyrolysis project layout. Projects launched in this period will come on stream in the first half of 2027, perfectly aligning with the surging demand for waste plastic treatment following the ban’s enforcement. With this forward-looking schedule, the project can fill the supply-demand gap in the European market. It will alleviate the EU’s pressing needs for waste plastic disposal while securing stable and sustainable project returns.

| Stage | Time | Core Tasks |

|---|---|---|

| Environmental Assessment & Permits | 8–14 months (Depends on countries) | Handle land procedures; obtain EIA approval |

| Upstream Supply (Waste Plastic Sourcing) | Concurrent (3-6 months) | Investigate waste plastic supply channels; sign long-term supply contracts |

| Downstream Disposal (Pyrolysis Oil Sales) | Concurrent (3-6 months) | Coordinate with petrochemical companies or traders; sign off-take agreements for pyrolysis oil |

| Financing | Concurrent (3-6 months) | Prepare project documents; apply for bank loans or investment |

| Equipment Procurement & Delivery | Concurrent (6-9 months) | Manufacture / logistics / installation / commissioning |

| Operation Launch | / | / |

4. Macro Value: Reshape Circular Economy and Environmental Resilience

Starting from November 21, 2026, the EU will impose a 30-month ban on plastic waste exports to non-OECD countries. Against this backdrop, the development of pyrolysis facilities and projects within the EU and non-OECD countries is of strategic significance for both sides.

4.1 For the EU

- Reshape the Domestic Circular Economy: Sstrengthen the EU’s local recycling industry, improve the waste plastic treatment system, and reduce external reliance.

- Enhance Recognition in Global Green Governance: halt cross-border waste shipments to fulfill environmental responsibilitie and establish a benchmark image of high-standard global environmental protection.

4.2 For Non-OECD Countries

- Cut off Pollution Pmports & Safeguard Environmental Security: The Waste Shipment Regulation (WSR) ban blocks waste transfers exported from the EU. It effectively reduces open-air waste burning, landfill leachate contamination and marine plastic pollution, and eases pressures on public health and ecological environments.

- Seize New Opportunities for Trade and Development: Following the 2029 regulatory adjustment, Non-OECD countries with compliant pyrolysis facilities will be legally eligible to receive EU plastic waste, gain substantial revenue from environmental services, and drive the upgrading of relevant industrial chains.

Conclusion

The implementation of export bans has completely reshaped the plastic recycling landscape. As a critical link connecting municipal solid waste and high-end chemical industries, highly compliant pyrolysis projects have demonstrated strong investment certainty. Facing the massive waste treatment gap emerging after 2026, securing substantial production capacity during the policy dividend period stands as the optimal choice for long-term asset appreciation.